First UAE bank to report Annual Pre-impairment Operating Profit above AED 10 billion Strong growth across all business units drives Net Profit up 58% to AED 5.1 billion Impaired Loan ratio improves to 7.8% with coverage ratio at 100.3% Proposed dividend increased to 35% from 25%

Dubai, 18 January 2015: First UAE bank to report Annual Pre-impairment Operating Profit above AED 10 billion Strong growth across all business units drives Net Profit up 58% to AED 5.1 billion Impaired Loan ratio improves to 7.8% with coverage ratio at 100.3% Proposed dividend increased to 35% from 25%

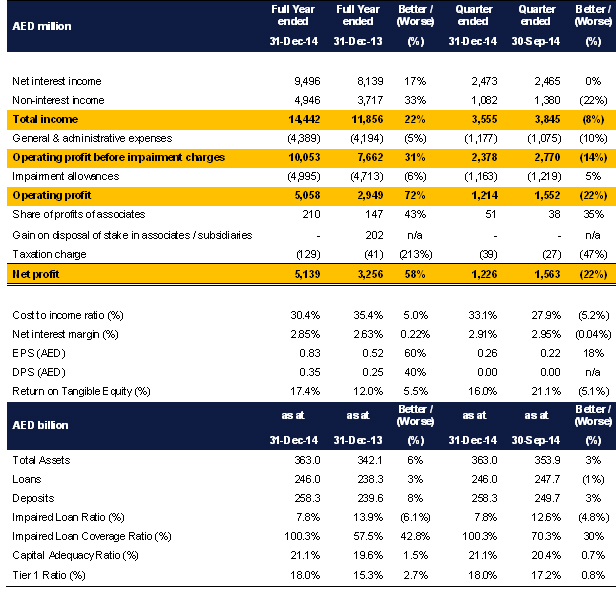

Financial Highlights

Emirates NBD (DFM: EmiratesNBD), the largest bank in the UAE by Total Income and branch network, delivered a strong set of financial results with net profit up 58% to AED 5.1 billion. The strong operating performance was helped by all parts of the business delivering year-on-year revenue growth. These impressive results have enabled the Board of Directors to recommend an increase in the 2014 dividend to 35 fils from 25 fils per share.

Total Income for the year 2014 grew by 22% to AED 14.4 billion. Net interest income grew 17% to AED 9.5 billion as asset growth was focused on higher margin Retail and Islamic products, whilst the Bank's liability profile improved thanks to current and saving account growth. Non-interest income grew 33% to AED 4.9 billion boosted by increased income from trade finance, foreign exchange and brokerage & asset management business as well as gains from the sale of property and investments.

The Bank's balance sheet strengthened further in 2014 thanks to an improvement in the capital, liquidity and credit quality ratios. The Bank's Impaired Loan ratio improved significantly to 7.8% in 2014. This improvement was due to the Bank's reclassification of its Dubai World exposure, the writing-off of fully provided retail loans and an increase in recoveries and repayments on the back of an improved economy. Further conservative provisioning of AED 5.0 billion helped boost the Impaired Loan Coverage ratio to 100.3%, reaching the Bank's target coverage level.

The Capital Adequacy ratio improved by 1.5% to 21.1% due to retained profits. The ability of the bank to attract and retain stable deposits helped improve the Advances to Deposit ratio by 4.3% to 95.2%.

Commenting on the Group's performance, His Highness Sheikh Ahmed Bin Saeed Al Maktoum, Chairman, Emirates NBD said: "2014 was a momentous year for Emirates NBD as we reached a number of key milestones. I would like to thank His Highness Sheikh Mohammed bin Rashid Al Maktoum, Vice President and Prime Minister of the UAE and Ruler of Dubai, for his vision, guidance and support that have greatly contributed to the success of Emirates NBD and Dubai. We are the first bank in the UAE, and for the first time in our 50 year history, to report an annual Operating Profit before Impairment in excess of AED 10 billion. This strong operating profit, coupled with conservative provisioning, has enabled Emirates NBD to reach 100% coverage ratio for impaired loans and successfully put legacy issues behind us. It is particularly pleasing that all the Group's business units delivered a strong performance in 2014. As a leading bank in the region, we are well placed to take advantage of future growth opportunities in Dubai, the UAE and the Gulf region. In light of the strong performance by the Bank, we are proposing to increase the cash dividend to 35 fils per share."

Mr. Hesham Abdulla Al Qassim, Vice Chairman, Emirates NBD said: "2014 saw Emirates NBD celebrate many major achievements. Net profit increased by 58% to AED 5.14 billion. This is driven by strong growth in both net interest income and non-interest income. It is important to note that each part of the business delivered year-on-year revenue growth. In light of the continued positive news on Dubai World the Bank was able to reclassify this exposure as performing. This helped us reach our 100% target coverage ratio for Impaired Loans. The Impaired Loan ratio improved to 7.8% during 2014 thanks to this reclassification and continued recoveries. The balance sheet strengthened further with a significant improvement in both the capital and liquidity ratios. Emirates NBD is well placed to take advantage of future opportunities in Dubai and the region."

Group Chief Executive Officer, Emirates NBD, Shayne Nelson said: "In my first full year as Group CEO, I am pleased to report that Emirates NBD delivered a strong set of financial results. 2014 saw a maturing of the Group's balance sheet and income statement. The Group's total Income grew by 22% due to increased volumes, a more profitable asset mix and a more efficient funding base. We were able to widen margins despite significant competition and liquidity has significantly improved in absolute and qualitative ratios. Costs remain firmly under control with a cost-to-income ratio of 30.4% for 2014, comfortably within our longer term target range. We continue to put the customer first with innovative products and excellent service. I am confident that the Bank will continue to deliver excellent customer service and superior value to our shareholders."

Financial Review

Total income for the year ended 31 December 2014 amounted to AED 14,442 million; an increase of 22% compared with AED 11,856 million in 2013.

Net interest income improved by 17% in 2014 to AED 9,496 million. The improvement in net interest income is attributable to an improved asset mix due to retail and Islamic growth, a lower cost of funds helped by both CASA growth and a reduction in relatively costly time deposits and a contribution from our Egyptian business.

Non-interest income for 2014 improved by 33% to AED 4,946 million, driven by increases in trade finance and foreign exchange income, brokerage & asset management fees and gains from the sale of property and investments.

2014 expenses amounted to AED 4,389 million, an increase of 5% over the previous year. This increase is due to staff and occupancy costs linked with rising business volumes and partially offset by a control of professional fees and marketing costs. The cost to income ratio improved by 5% y-o-y to 30.4%, as improving top line momentum more than offset the increase in costs. Excluding one-offs, the cost to income ratio would have been 31.3%.

During 2014 the Impaired Loan ratio improved to 7.8%. This improvement is due to a reclassification of the Bank's Dubai World exposure, the write-off of fully provided retail loans, and a sharp rise in repayments and recoveries as a result of a stronger economy and a more vigorous pursuit of problem loan resolution. The 2014 impairment charge increased to AED 4,995 million. This was driven by conservative provisioning on the Corporate and Islamic Financing portfolios, which helped boost the coverage ratio to 100.3% and enabled the Bank to reach its coverage target and put behind its legacy issues.

Net profit for the Group was AED 5,139 million in 2014, 58% above the profit posted for 2013. The increase in net profits was driven by growth in both net interest income & non-interest income outpacing the rise in expenses and provisions.

Deposits increased by 8% and gross loans grew by 3% during 2014. Gross loans grew by 5% if we exclude the write-off of fully provided for retail loans. The Advances to Deposits Ratio strengthened by 4.3% in 2014 to finish the year at 95.2%, thanks to the Bank's on-going ability to attract and retain economical current and saving account deposits.

As at 31 December 2014, the Bank's capital adequacy ratio and Tier 1 capital ratios were 21.1% and 18.0% respectively. The 2.7% improvement in the Tier 1 ratio recorded in 2014 is due to retained profit coupled with a $500 million Tier 1 issue.

Business Performance

Retail Banking & Wealth Management (RBWM)

The Retail Banking and Wealth Management division continued to perform strongly in 2014, growing at a faster rate than the market in key product groups.

Revenues grew 8% to reach AED 5,621 million in 2014. Commission and fee income have become a major source of revenue for RBWM, and now accounts for more than a third of all income. RBWM built up additional liquidity in 2014 through low cost current and savings accounts. Deposits grew 12% in 2014 to reach AED 113.5 billion, strengthening the Banks's market leading position in the UAE.

RBWM's strategy of effective customer acquisition is bearing strong results with higher revenues per customer, lower provisions and better product penetration levels. In 2014 the Bank launched "Beyond from Personal Banking" which targets emerging affluent customers, a sector which represents 20% of the UAE's banking population. The Business Banking segment continued to experience healthy growth, driven by trade finance, lending and forex offerings. Revenues from both wealth and asset-management products also increased significantly.

The bank's partnerships with global brands such as Skywards and Manchester United continued to drive strong growth in credit cards and other products. The DirectRemit service launched in 2014 offers instant remittances to the two largest remittance markets of India and Philippines, with service to additional countries planned for 2015.

Our best-in-class online and mobile banking solutions have been effective in dealing with higher volumes of routine transactions resulting in improved customer service and lower operational costs. RBWM also launched various innovative services such as the e-IPO platform for digital subscription to IPOs.

Emirates NBD Private Banking showed strong growth in its core segments across the UAE, Saudi Arabia, Singapore and UK. Emirates NBD Asset Management is now recognized as a leading asset manager in the UAE with over AED 10 billion in assets under management. Emirates NBD Securities, the brokerage arm of the Group, improved its market position in 2014 as it saw trading volumes grow by 14% during the year.

Wholesale Banking (WB)

Wholesale Banking delivered a strong performance for 2014 with operating income at AED 4.82 billion, up by 8% compared with 2013.

Net interest income of AED 3.51 billion was 10% higher for 2014 due to asset growth and yield management.

Fee income increased by 5% to AED 1.31 billion in 2014 reflecting a strong performance in trade finance, foreign exchange and Investment Banking business.

The Investment Banking platform – Emirates NBD Capital Ltd – continued its strong performance. During the year it acted as joint lead arranger and book runner for USD 8.1 billion worth of loan syndication and capital market transactions and was ranked as the highest Middle East arranger and number 3 globally, of US dollar sukuk issuances.

Global Markets & Treasury (GMT)

GMT reported an 81% increase in total income to AED 835 million for 2014.

The strong performance is a result of an increase in Net Interest Income due to effective balance sheet positioning and hedging. The numbers also reflect strong revenue growth from Treasury Sales, a solid performance in the Investment portfolio & Credit Trading delivered another exceptional performance in 2014.

Global Funding issued a number of successful public bonds including a US$ 500m Tier 1 capital issue and a US$ 1 billion 5-year senior issue as well as further public issues in Australian Dollars and New Zealand Dollars. Global Funding also issued nearly US$ 1 billion in private placements in a range of currencies.

GM&T expects Sales & Trading revenues to be strong in 2015 on the back of improved economic conditions in US, continued optimism in our home markets, and providing a wider product offering to clients looking to hedge their financial markets exposures due to enhanced volatility.

Emirates Islamic (EI)

EI continued to deliver a healthy performance as total income (net of customers' share of profit) grew by 28% to AED 1.95 billion in 2014. Financing and investing receivables grew by 20% to AED 26.1 billion during the year. The Bank continued its expansion of Branch network by opening 6 new branches in 2014.

EI's net profit grew by 161% to AED 364 million for 2014.

EI aspires to become the leading Islamic Bank in the UAE. EI's management aims to increase market share whilst building a strong and sustainable customer base. EI's focus in 2014 has been on growing the SME portfolio supported by an increased product offering. EI's success was recognized by winning the Best Premium Islamic Card and Best Self Employed Finance from CPI Financial in 2014.

Emirates NBD Egypt

For its first full calendar year as an Emirates NBD entity, our Egypt operations delivered a robust performance. Total revenues grew 16% in 2014 to AED 706 million, while costs remained under control. With more than 1,500 employees, the bank reached a net profit of AED 232 million. Deposits increased by 16%, while gross loans expanded by 5% during 2014, reaching AED 10.2 billion and AED 3.8 billion, respectively. The integration of Emirates NBD Egypt is well on track, with our Cairo head office and 61 branches across the country having been fully re-branded.

We have witnessed sound business growth during 2014 in our retail loan portfolio, while maintaining strong credit quality.

Emirates NBD Egypt has moved up one notch in 2014 to become the 8th largest privately owned bank in Egypt both in terms of balance sheet size and profitability.

Outlook

The UAE remains well-positioned to enjoy solid growth in 2015 driven primarily by an expansion in non-oil sectors, particularly manufacturing, transport, logistics and construction. We expect tourism to remain an important contributor to growth notwithstanding more challenging conditions in key markets such as Russia. Following the recent fall in oil prices, the Bank has adjusted its 2015 UAE growth forecast down to 4.3% (from 4.8%). The bank forecast for 2015 GDP growth in Dubai is 4.7%. The Bank has strengthened its balance sheet thanks to improvements in capital, liquidity and credit quality. This provides a solid platform to take advantage of growth opportunities in Dubai and the region. This strategy is built around five core building blocks which include delivering excellent customer experience, building a high performance organisation, driving core businesses, running an efficient organisation and diversifying sources of income.

UAE

UAE