Emirates NBD (DFM: EmiratesNBD), a leading banking group in the region, delivered a net profit of AED 7.0 billion in 2020 despite a challenging operating environment.

- Total income of AED 23.2 billion improved 4% y-o-y

- Total Assets up 2% y-o-y to AED 698 billion

- Operating Profit of AED 7.4 billion, 29% lower on higher provisions

- Proposed dividend of 40%

Dubai, 27 January 2021

Emirates NBD (DFM: EmiratesNBD), a leading banking group in the region, delivered a net profit of AED 7.0 billion in 2020 despite a challenging operating environment. Total income increased 4% y-o-y as the positive contribution from DenizBank helped offset a decline in net interest margin due to lower interest rates and a reduction in non-funded income. Emirates NBD provided support to over 103,000 customers in the UAE, and provided assistance to many customers in the other geographies in which the Bank operates. Emirates NBD further enhanced its digital products and services as an increasing number of customers embraced this secure and convenient way of banking. The Group’s balance sheet remains healthy with strong capital, liquidity and impaired loan coverage ratios. These results have enabled the Board of Directors to recommend a 2020 dividend of 40 fils per share.

Financial Highlights – FY 2020

- Total income of AED 23.2 billion improved 4% y-o-y on loan growth, including DenizBank

- Net profit of AED 7 billion declined 52% y-o-y on higher provisions and gain from sale of Network International shares not repeated in 2020. Excluding the Network International gain in 2019, net profit was down 31% y-o-y

- Impairment allowances increased to AED 7.9 billion reflecting weaker credit environment impact of Covid-19 with net cost of risk at 163 bps

- Net interest margin declined 24 bps y-o-y to 2.65% following cuts in base interest rates in the first half of 2020

- Total assets at AED 698 billion, up 2% from 2019

- Customer loans at AED 444 billion, up 1% from 2019

- Customer deposits at AED 464 billion, down 2% from 2019

- Non-performing loan ratio increased 0.6% to 6.2% in 2020 and coverage ratio remained strong at 117.3%

- Liquidity coverage ratio of 165% and advances to deposit ratio of 95.6% demonstrate a healthy liquidity position

- Common equity tier 1 ratio of 15.0%

Commenting on the Bank’s performance, His Highness Sheikh Ahmed Bin Saeed Al Maktoum, Chairman, Emirates NBD said: “Emirates NBD delivered a net profit of AED 7 billion in 2020 despite the global pandemic that caused major disruption to individuals, communities and businesses. The swift and decisive action of the UAE’s wise leadership in protecting the health of residents with clear and measured guidelines allowed the UAE economy to successfully reopen in the second half of the year. The Central Bank of the UAE’s Targeted Economic Support Scheme has been instrumental in helping customers and banks through these challenging times. I am proud that Emirates NBD played its part in supporting customers and the economy by providing financial assistance as well as actively participating in community initiatives. We continue to support the economy of the UAE as it proudly celebrates its golden jubilee in 2021 and we are excited to play an important role in the UAE’s further development over the next fifty years. As the official banking partner of Expo 2020 Dubai, we look forward to helping showcase the UAE’s innovative, tolerant and proud culture as we welcome the world to the UAE. In light of the Bank’s performance, we are proposing a cash dividend at 40 fils per share.”

Hesham Abdulla Al Qassim, Vice Chairman and Managing Director, Emirates NBD said: “Emirates NBD’s strong balance sheet, coupled with the ongoing ability to generate operating profit, enabled the Bank to successfully deal with the unforeseen challenges in 2020, achieving a net profit of AED 7 billion and growing total assets to AED 698 billion. The measures introduced by the Central Bank of the UAE, through the Targeted Economic Support Scheme have significantly helped support the financial wellbeing of individuals and businesses. The UAE banking system remains in good health thanks to the proactive measures taken by the UAE Government and the Central Bank of the UAE. Emirates NBD has further cemented its reputation for innovation in products and service in the fourth quarter with the unveiling of businessONLINE, providing corporate clients with a, seamless, secure and agile single-window to support all their banking needs. We also launched the E20. Digital Business Bank which simplifies banking for start-ups, entrepreneurs and SMEs. We are honoured to be named ‘Bank of the Year – UAE 2020’ for the sixth year and ‘Bank of the Year – Middle East 2020’ for the third time by The Banker, recognising the Bank’s efforts in responding to the global pandemic and its innovate approach to digital banking. In addition, Emirates NBD has been assessed as the ‘Strongest Bank in the UAE’ and ‘Fifth Strongest Bank in the Middle East’ by The Asian Banker 500 Largest and Strongest Banks Rankings.”

Commenting on the Bank’s performance, Shayne Nelson, Group Chief Executive Officer said: “Emirates NBD delivered a 1% improvement in pre-impairment operating profit in 2020 despite a challenging operating environment. Net interest income increased by 8% during the year as the contribution from DenizBank more than offset a decline in margins due to lower interest rates. Operating profit was 29% lower mainly due to lower interest rates & transaction volumes, coupled with higher impairment allowances. Emirates NBD’s resilient operating performance, coupled with a solid balance sheet will provide a platform for customers to take advantage of growth opportunities in the year ahead. Customer banking preferences changed during 2020 as an increasing number of both retail and corporate customers embraced digital banking. Emirates NBD’s significant investment in digital and technology over the last four years allowed the Bank to seamlessly adjust to this change in customer banking behaviour. We have provided interest and principal deferral support to over 103,000 customers in the UAE. Many other customers have benefited through waiver of fees and other support, both within the UAE and in the other geographies we operate in. The safety and well-being of our customers and employees remains our top priority. Following a challenging 2020, the expectation for economic growth in the countries that we operate in is more optimistic.”

Financial Review

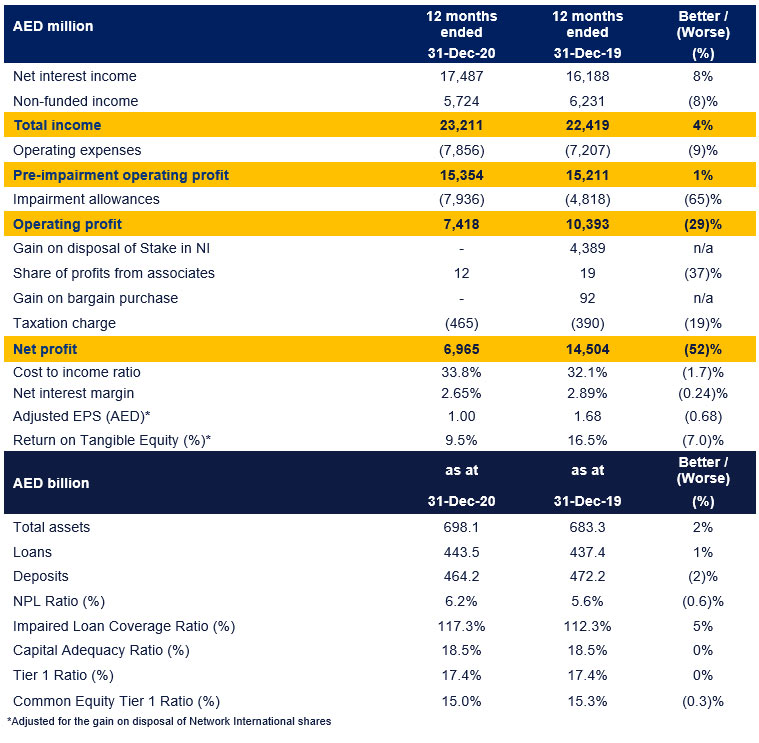

Total income for 2020 amounted to AED 23,211 million, an increase of 4% compared with AED 22,419 million in 2019. Net interest income improved 8% y-o-y as the contribution from DenizBank more than offset a decline in margins due to lower interest rates. Excluding DenizBank, net interest income declined 13% y-o-y due to lower margins.

Total non-funded income declined by 8% y-o-y on lower fee-based activity due to the impact of Covid-19. Excluding DenizBank, non-funded income declined 19% on lower volumes from subdued business activity. Operating profit declined 29% y-o-y mainly due to lower interest rates & transaction volumes, coupled with higher impairment allowances.

Costs for 2020 increased by 9% to AED 7,856 million due to the full-year inclusion of DenizBank. Excluding DenizBank, costs improved 6% y-o-y as a result of management actions during 2020 in response to Covid-19 and lower income. The cost-to-income ratio at 33.8% in 2020, is broadly near long term guidance.

During 2020, the Non-Performing Loan Ratio increased to 6.2%. The impairment charge during this period of AED 7,936 million is 65% higher y-o-y as Stage 1 & 2 coverage increased.

The Group’s net profit of AED 6,965 million in 2020 is 52% lower than in 2019. The decline in net profit was driven by higher provisions and no repeat of the gain on disposal of Network International shares in 2019. Net profit was down 31% excluding the Network International gain in 2019.

Loans increased by 1% during 2020 while Deposits were down 2% mainly due to a lower AED contribution from DenizBank. Liquidity remains strong with the Liquidity Coverage ratio at 165% as at 31 December 2020 and the Advances to Deposits Ratio at 95.6%. During 2020, the Group raised AED 18.4 billion of senior term funding in seven currencies including three benchmark senior public bond & sukuk issues and private placements with maturities out to 30 years.

As at 31 December 2020, the Group’s Common Equity Tier 1 ratio is 15.0%, Tier 1 ratio is 17.4% and Capital Adequacy ratio is 18.5%.

Business Performance

Retail Banking & Wealth Management (RBWM)

RBWM’s pre-impairment operating profit remained resilient in 2020, declining only 1% despite the challenging operating environment. Total income of AED 7,764 million was 5% lower than the previous year. Net interest income remained flat aided by strong balance growth countering the impact of downward rate movements. Non-funded income was down 15% on reduced economic activity due to Covid-19.

Operating costs of AED 2,050 million were 10% lower as cost management initiatives took effect. Stage 1 & 2 impairment allowances increased resulting in a 14% decline in net profit. Credit quality of the newly originated retail book remains robust.

Liabilities grew by 8% or AED 11.8 billion during the year led by strong Current & Savings Accounts growth and supported by marketing campaigns. Customer advances improved during the second half of 2020 to end 2% ahead of the previous year. A series of relief measures were rolled out to support customers. Instalment holidays were provided to about 10% of its customer base and a debt restructuring program, offering reduced monthly instalment, was offered to customers experiencing salary disruption.

The Cards business launched the Emirates NBD Visa Flexi Credit Card, a global first allowing customers to personalize their credit card with benefits to match their lifestyle. The Emirati Debit Card was launched offering UAE National customers a range of exclusive benefits.

Digital usage continued to rise with over three-quarters of RBWM customers now digitally active and over 85% of point-of-sale card transactions now contactless. The Mobile Application and website capabilities were enhanced making it easier for customers to sign up digitally for new products and services.

Liv., the lifestyle digital bank for millennials, introduced credit card and personal loan products, as its customer base, crossed 400,000 customers in the UAE and extended into the KSA market. The E20. digital business bank was rolled out to the market, enabling start-ups, entrepreneurs and SMEs to manage their banking needs conveniently through a mobile application.

Private Banking grew total income by 1%, led by a 33% increase in fee income. Video based meetings and virtual investment webinars were conducted during the year to update customers on market and portfolio performance. Emirates NBD Asset Management launched the Emirates Signature multi-asset funds, offering customers a cost-effective product with global exposure to suit investors’ profile and time horizon.

Corporate & Institutional Banking (C&IB)

C&IB delivered total income of AED 5,922 million for 2020, 5% lower compared to 2019. Net profits were flat to 2019 due to lower income which was offset by lower impairment allowances.

Net interest income of AED 4,571 million for 2020 was 4% lower than the previous year as lending growth helped mitigate margin compression due to lower interest rates.

Fee income of AED 1,351 million for 2020 declined 7% compared to 2019 as lower economic activity affected lending fee and commission income although this was partially offset by higher income from investment banking and treasury sales.

Costs for 2020 were 4% lower compared with 2019 as cost management actions took effect.

The credit quality of newly originated business continued to be stable. Net impairment allowances were lower for 2020 despite lower recoveries and higher impairment allowances on Stage 1 & 2 loans as a corporate debt restructuring improved the credit profile.

In terms of balance sheet, assets grew by 1% mainly due to growth in lending activity. Liabilities were 11% higher with a continued focus on growing CASA.

C&IB launched a number of key products to support customers’ increased appetite for secure and convenient banking solutions. C&IB unveiled its next-generation global corporate banking platform, ‘businessONLINE’, supporting clients’ banking needs across geographies through a single-window, seamless, secure and agile platform. businessONLINE delivers a full suite of cash management, trade finance and liquidity management solutions to customers. businessONLINE integrates with multiple technology partners, providing one-stop access through a suite of accounting, sales, inventory, purchasing and customer relationship services.

We continue to provide support to customers across all key sectors to cope with the business disruption caused by Covid-19, including interest and principal deferral relief for up to six months and reduced bank charges on transactions through digital channels.

Global Markets & Treasury (GM&T)

GM&T interest income declined in 2020 following the significant interest rate cuts in the first half of the year.

The Trading desks delivered a solid performance successfully navigating heightened volatility in foreign exchange, interest rates and credit markets with Credit Trading delivering an outstanding performance helped by higher new issuance volumes in the region.

The Sales & Structuring team was proactive in offering derivative solutions to customers towards hedging long dated interest rate exposures to capitalize on record low rates.

The Global Funding Desk raised AED 16.6 billion of term funding in 2020, including two benchmark senior public bond issues and AED 13.0 billion of private placements with maturities out to 30 years. Emirates Islamic also raised AED 1.8 billion through a public Sukuk issue.

GM&T successfully completed a LIBOR transition impact analysis and enhanced infrastructure to support the UAE Central Bank’s Dirham Monetary Framework initiative.

Emirates Islamic (EI)

EI reported a net loss of AED 482 million in 2020 mainly due to higher impairments on its financing and investment book. EI’s total income of AED 2.1 billion declined 22% during the year due to lower income from financing receivables and investments and lower fee and commission income due to the impact of Covid-19 on economic activity. EI successfully issued a AED 1.8 billion benchmark Sukuk during 2020.

EI’s total assets reached AED 70.6 billion at the end of 2020. Financing and Investing Receivables increased by 9% to AED 40.8 billion during the year and Customer accounts grew by 3% to AED 46.9 billion. CASA balances represented 69% of total customer accounts. EI’s headline Financing to Deposit ratio stands at 87% and is comfortably within the management’s target range.

DenizBank

DenizBank contributed total income of AED 7,257 million and net profit of AED 1,369 million to the Group for 2020. It had total assets of AED 131 billion, net loans of AED 81 billion and deposits of AED 85 billion at the end of 2020. DenizBank is the fifth largest private bank in Turkey with a wide presence through a network of 730 branches and over 3,100 ATMs. It operates with 695 branches in Turkey and 35 in other territories (Austria, Germany, Bahrain) servicing more than 14 million customers, through over 14,000 employees.

Outlook

Following a strict lockdown during the second quarter of 2020, the UAE Government’s clear guidelines enabled the UAE economy to re-open in the second half of 2020. Emirates NBD’s Research team forecasts that the UAE economy contracted by 6.9% in 2020, as both oil and non-oil sectors were impacted by coronavirus. However, Emirates NBD Research expects real GDP growth for 2021 to recover to 3% in Dubai and 1.9% in the UAE, with the non-oil sector expected to grow by 3.5%. Economic growth is also expected to return to other countries where Emirates NBD has a presence.

UAE

UAE