Net profits up 8% to AED 1.8 billion on higher income and lower provisions

Net profits up 8% to AED 1.8 billion on higher income and lower provisions

Dubai, 19 April 2016:

Financial Highlights

Emirates NBD (DFM: EmiratesNBD), the UAE’s largest lender, delivered a solid set of financial results with net profit up 8% to AED 1.8 billion. The healthy operating performance was helped by an increase in total income, driven by asset growth and stable core fee income, coupled with a control on expenses and lower provisions. Despite challenging market conditions, Emirates NBD continued to achieve growth in revenue and net profit as various parts of the business delivered a robust performance in the first quarter.

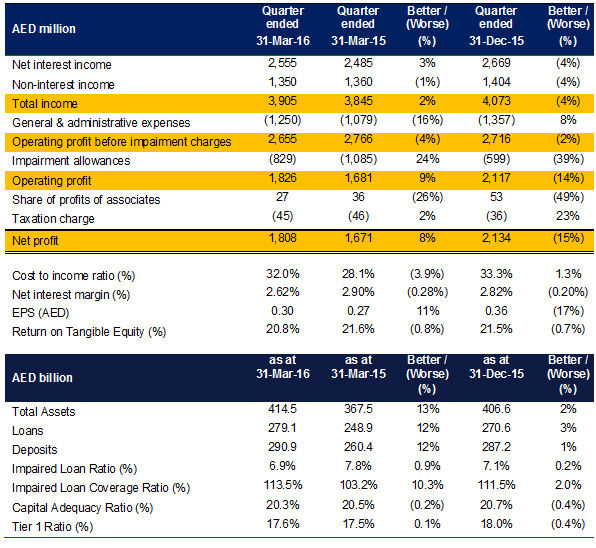

Total Income for the first quarter grew by 2% to AED 3.9 billion. Net interest income grew 3% to AED 2.6 billion as loan growth more than offset a contraction in margins. Non-interest income marginally declined by 1% to AED 1.4 billion as core fee income held steady, bolstered by growth in credit card volumes, whilst income from property and investments declined due to lower one-off gains.

The Bank’s balance sheet remained strong in Q1-16. Credit quality improved as the Impaired Loan ratio advanced from 7.1% to 6.9% during the quarter whilst the Impaired Loan Coverage ratio also strengthened to 113.5%. The Bank’s Advances to Deposit ratio at 95.9% remains comfortably within the management’s target range. During the quarter the Bank issued AED 2 billion of term debt through private placements at competitive pricing which further boosted structural liquidity. Capital Ratios, at a healthy 20.3%, reduced slightly in Q1 as the annual dividend payment more than offset retained profit in the quarter. As with previous years it is expected that retained profit will grow the capital base throughout the remainder of the year.

Commenting on the Group’s performance, Mr. Hesham Abdulla Al Qassim, Vice Chairman, Emirates NBD said: “I am very pleased with the solid performance that Emirates NBD has delivered in the first quarter of 2016 despite ongoing concerns about global growth. In Q1 2016 Emirates NBD achieved an 8% growth in net profit to AED 1,808 million. The balance sheet continues to remain strong, with further improvements in credit quality metrics coupled with steady funding and capital ratios. The Group is well positioned to utilise our strong franchise, capital and liquidity base to take advantage of opportunities within the region.”

Group Chief Executive Officer, Shayne Nelson said: “I am pleased that we have delivered another robust set of financial results with a net profit of AED 1,808 million, up 8% compared to the same quarter in 2015. This is driven by higher income from asset growth and lower provisions. Liquidity pressures in the sector continued to ease in the first quarter from the tight conditions experienced in the second half of 2015. Wholesale Banking, Global Markets & Treasury and Retail Banking & Wealth Management units all delivered a solid first quarter. We remain cautiously optimistic for the remainder of 2016 but are conscious of the headwinds that a strong dollar and volatile oil price can present.”

Group Chief Financial Officer, Surya Subramanian said: “The operating performance for the first quarter of 2016 improved, as demonstrated by the growth in both total income and net profit. We remain very focused on controlling expenses and our structural liquidity remains sound. We were able to raise AED 2 billion of term funding through private placements at competitive pricing, despite challenging market conditions.”

Financial Review

Total income for the quarter ended 31 March 2016 amounted to AED 3,905 million; an increase of 2% compared with AED 3,845 million during the same period in 2015.

Net interest income improved by 3% in Q1-16 to AED 2,555 million. The improvement in net interest income is attributable to overall loan growth which helped offset a contraction in margins.

Non-interest income for the period marginally declined by 1% to AED 1,350 million as core fee income held steady due to growth in credit card volumes, and income from property and investments declined.

Costs for the quarter ended 31 March 2016 amounted to AED 1,250 million, an increase of 16% over the previous year due to higher staff costs linked with increased business volumes. Costs did improve by 8% compared to the last quarter of 2015. The cost to income ratio rose by 3.9% y-o-y to 32.0%. Excluding one-offs, the cost to income ratio would be 33.6%.

During the quarter, the Impaired Loan Ratio improved further to 6.9% from 7.1% at the end of 2015. The impairment charge in Q1-16 of AED 829 million is 24% lower than in Q1-15 as the cost of risk continues to normalize. This net provision includes AED 226 million of write-backs and recoveries, and together helped boost the coverage ratio to 113.5%.

Net profit for the Group was AED 1,808 million in Q1-16, 8% above the profit posted in Q1-15. The increase in net profit was driven by growth in net interest income, a control on expenses and reduced provisions.

Loans increased by 3% and Deposits grew by 1% during the quarter. The Advances to Deposits Ratio is at 95.9%. During the quarter the Bank prudently replaced AED 1.5 billion of maturing debt with AED 2.0 billon of term funding raised through private placements.

As at 31 March 2016, the Bank’s capital adequacy ratio and Tier 1 capital ratio were 20.3% and 17.6% respectively.

Business Performance

Retail Banking & Wealth Management (RBWM)

RBWM reported an operating income of AED 1,513 million for the first quarter of 2016, up 8% from the previous year. Net interest income grew 6% to AED 918 million while fee income rose 11% to AED 595 million, led by growth in foreign exchange remittance, Wealth Management and the credit card business. Fee income now accounts for 39% of total income.

Revenue growth was driven by a further improvement in the funding mix. Current Account & Savings Account (CASA) balances grew by AED 5.2 billion in Q1 2016, and represent 84% of total deposits. RBWM continues to focus on sourcing higher value customers through the “Beyond” and Priority Banking proposition via the recently launched Salary Transfer Promotion.

The Cards business experienced double digit growth in card spend year-on-year, reinforcing the Bank’s position as the leading cards business in the UAE. RBWM’s focus remains on the premium cards segment, with the recently launched Emirates NBD Starwood Preferred Guest credit card and a new 75,000 miles promotion for its flagship Emirates NBD Skywards credit card.

The Bank continues to invest in digital initiatives to improve customer engagement and experience. During the quarter, the Bank launched the next generation of Interactive Teller Machines and expanded its mobile banking app with new products and features such as instalment plans and instant loans. Emirates NBD was ranked 17th globally amongst banks by Financial Brand for Social Media in Q1 2016.

Wealth Management, and in particular Private Banking, had a strong first quarter in 2016, with revenue growth driven by investment-related fee income. Wealth Management also expanded its client coverage scope to target high and ultra-high net worth clientele in East & West Africa, as well as family offices and other institutional-type investors.

Emirates NBD Asset Management maintained its regional leadership position with Assets under Management growing to nearly AED 12 billion during the quarter, whilst Emirates NBD Securities improved its market position despite an overall low-volume trading environment.

Wholesale Banking (WB)

Wholesale Banking, delivered a strong performance for the quarter ended 31 March 2016 with net profit of AED 705 million; up 41% compared with net profit of AED 499 million for the quarter ended 31 March 2015; backed by continuing momentum in the core business and lower provisioning requirements due to improvement in the credit quality of the loan book.

Net interest income of AED 778 million for the quarter ended 31 March 2016 was lower by 13% compared with AED 898 million for the quarter ended 31 March 2015, mainly due to re-alignment in internal management reporting together with interest margin compression.

Fee income of AED 317 million for the quarter ended 31 March 2016 was lower by 9% compared with AED 349 million for the quarter ended 31 March 2015, mainly on account of lower transaction related fees due to slower market conditions.

Costs were up by 34% compared with the previous period ended 31 March 2015 mainly due to organizational re-alignment, an increase in cost of distribution network usage and selective initiatives undertaken to reshape the business. Wholesale Banking continues to invest in upgrading its Transaction Banking systems to improve levels of straight through processing and in Global Markets & Treasury (GM&T) systems where upgrades will support the Bank’s recent significant enhancement in GM&T product capability.

The credit quality of the loan book remained strong resulting in a 58% improvement in provisioning requirements to AED 280 million, compared to AED 664 million for the quarter ended 31 March 2015.

Asset balances remained broadly flat during Q1-16 as new bookings were offset by repayments. Deposits were lower by 3% reflecting efforts to reduce more expensive time deposits whilst maintaining liquidity at optimum levels.

Wholesale Banking continues to make good progress in its transformation programme aiming to become the leading Wholesale Bank in the Middle East and North Africa by providing a full range of Wholesale Banking products and solutions to the Bank’s customers across the Region.

Global Markets & Treasury

Global Markets & Treasury reported total income of AED 159 million for the quarter ending 31 March 2016. Net Interest Income benefited from a combination of the US rate hike in December, cheaper interbank funding costs during the first quarter and a change in internal transfer pricing.

This growth in income was driven by a good performance across all products within GM&T.

Sales revenues grew 16% as the business unit witnessed higher volumes in Interest Rate hedging products, Foreign Exchange & Fixed Income sales.

Trading and Investment revenues improved as both Credit Trading and Foreign Exchange Trading delivered a strong performance despite challenging market conditions.

Global Funding issued AED 2 billion of term debt through private placements which more than replaced the AED 1.5 billion that matured in Q1 2016.

Emirates Islamic (EI)

EI delivered a robust performance in Q1 2016 with an increase in customer assets, deposits and core income during the first three months of 2016.

Financing and Investing Receivables growing 9% to AED 37 billion during the quarter. EI’s continued and focused approach to improve its liabilities mix also led to a significant increase in CASA balances in Q1 2016.

The net profit for the first quarter of 2016 is AED 45 million. Adjusted for one offs, total income in Q1 2016 increased by 15% compared to the same period last year due to growth in the financing book, effective margin management and increased fee income.

The NPL ratio improved to 8.6% during the quarter, with the coverage ratio rising to 91%. With proactive credit risk management and a conservative provisioning policy, EI was able to maintain the quality of its asset book amid challenging market conditions.

EI expanded its branch network to 61 by adding one new branch during 2016. In order to enhance customer banking experience, EI also added nine new ATMS & SDMs, bringing the total number to 199.

Outlook:

Emirates NBD estimates UAE economic growth at 4.0% in real terms in 2015, down from 4.6% in 2014. We expect growth to slow further to 3.0% this year as lower oil prices are likely to contribute to a tighter fiscal policy and slower non-oil sector growth. Tighter liquidity conditions and a strong dollar will continue to pose headwinds to non-oil growth, particularly in the services sectors. However, oil output is expected to rise in line with official targets and this should help to boost headline GDP growth. The Bank will continue to implement its successful strategy built around five core building blocks which include delivering excellent customer experience, building a high performance organisation, driving core businesses, running an efficient organisation and diversifying sources of income.

UAE

UAE